Russian Financial Crisis of 2014

By the end of year 2014, Russia witnessed a crash in the financial market due to a sudden fall in the oil prices and also due to sanction wars. This led to the reduction in the domestic demand, devaluation of the Russian ruble and also caused high inflation in the country. The lowering of the exchange rate creates a possibility of offsetting the reduction in domestic demand through increased exports. However, this article aims at understanding the crisis in general; the causes for the crisis and the impacts of it at a macroeconomic level, taking into account the structural problems of Russia which led to more severe consequences than anticipated. It aims at empirically analyzing the crisis; developing an understanding of the policies and tactics adopted by the government to overcome the crisis and coming up with recommendations that would help in speedy recovery of the Russian economy.

Introduction

In December 2014, the stock exchange of Moscow witnessed the fragility and the unpredictability of the financial system of the Russian Federation. The USD as well as the Euro exchange rates suddenly rose to an all time high level of 80 and 100 ruble per unit of currency, respectively. The collapse of the Russian ruble was the apex of the continuing depreciation in the preceding months in Russia. The crisis was caused mainly because of the decreasing oil prices and because of the conflicts between Russia and the Western countries over the insistent aggressive policy adopted by Moscow towards Ukraine.

Moreover, the Russian ruble was hit by a continuous series of changes which resulted in the destabilization of the country’s financial market. Among these changes, the most important one was the increase in demand of the Russian ruble as the deadline for the repayment of a huge installment of a foreign-lend loan approached. Another important one was the reduction in the confidence of the market players on the Central Bank of Russia’s (CBR) policy, the reason of this being the inefficiency of CBR in dealing with inflation and defending the ruble exchange.

The CBR also made a prediction in December 2014 about a serious recession in the country in 2015. This undoubtedly worsened the entire situation. What is remarkable is the fact that the Russian ruble crashed while the oil prices were declining faintly even if steadily. The consumers also began to withdraw deposits whereas some banks feared liquidity loss and limited the amount of withdrawal.

Literature Review

Literature show that many financial crises have occurred in the past in Russia, the most important of them being the Russian financial crisis of 1998 and that of 2009. One of the impacts of the 2014 financial crisis was the devaluation of Russian ruble which resulted in inflation and fall in the GDP growth rate.

Although devaluation is often considered to be an incentive for economic growth, authors of various papers now have a skeptical outlook towards the positive impacts of devaluation. (Gylfason and Schmid, 1983) Authors now talk about what is known as “devaluation pessimism” which was first given by Cooper in 1969 and which provides the basis of studying the impact of devaluation on the aggregate demand and money supply in the economy.

Kamin (1988) in one of his papers noted a sharp slowdown in the GDP growth which began a year before devaluation actually took place and continued over the year when the devaluation actually took place. This is exactly what happened in the financial crisis of Russia in 2014 as there was a pre-devaluation slowdown in GDP growth. (Bussière, Saxena and Tovar, 2012) A number of works actually proves that devaluation does not act an efficient tool for growing the GDP especially in the short or medium term especially in developing countries. (Calvo and Reinhart, 2000; Frankel, 2005)

The problems that countries usually face after devaluation are- degradation of country’s credit rating, high volatility of the real exchange rate, closure of access to international financial market and high inflation. (Calvo and Reinhart, 2000) Moreover, the impacts of the devaluation of currency are country specific. (Gupta, Mishra and Sahay, 2007) Thus the adverse impacts of devaluation of currency or financial crisis like the Russian crisis of 2014 are- decline in aggregate demand and GDP of the country ( Diaz-Alejandro, 1963); rise in the inflation in the country (Frankel, 2005) and low export and import price elasticity which might lead to recession. (Blank, Gurvich and Ulyukaev, 2006)

Although devaluation is often considered to be an incentive for economic growth, authors of various papers now have a skeptical outlook towards the positive impacts of devaluation. (Gylfason and Schmid, 1983) Authors now talk about what is known as

Causes of the Crisis

1. The deteriorating structural problems of the Russian Economy – The structural problems of the economy of Russia were a result of the Russian Economy attaining the boundaries of its potential. Because the economy of Russia relies on the mining and export of energy resources that accounts for around 20% of GDP, 70% of revenues from export and also for almost 50% of its budget revenues, it resulted in highly vulnerability of the economy to the instabilities in the global market of oil. The easy way to earn money from the oil exports has for decades undermined any incentive the Russian government could do to encourage more high-technological branches of industry as a result of which the export and budget revenue of the country crippled , making it tough for the government to stabilize its export and budget revenue.

2. Sanction wars and serious tensions in the relations of Russia with the West -The serious tension in the relations of Russia and the West because of Russia’s capture of Crimea and the country’s military actions in Ukraine affected the economy of Russia by drastically undermining its image globally and also provoking a “sanction war”. The reaction of the capital markets to Russia’s aggressive move towards Ukraine demonstrated the quick and politically encouraged loss of trust on Russia internationally which resulted in a higher capital outflow from the country and resulted in a substantial loss in the stock exchange market . The investment and the credit worthiness of Russia were further weakened by the economic sanctions imposed by the West in a reply to Russia’s destabilization of Ukraine. The significance of the sanctions imposed became a problem for Russia later because of the fact that the country had to repay a large amount of its debt of around US$ 35 billion. In a situation where it was cut off from Western World and its currency had lost much of its value it became one of the major reasons behind the crash in its financial markets and also affected the economic stability of the country. The country’s economic situation deteriorated further because of the reactive measures it applied that like the embargo on the imports of many agricultural goods and food products from western countries that had imposed the initial sanctions. The result was shortage in market, along with little developed domestic production and the excessive cost of importing food from other alternative sources. This caused the average rate of inflation in the food sector to reach a record high of 15.4%.

3. Drastic slump in the oil prices -The slump in the prices of oil in international market n the end of 2014 by more than 50 percent (from US$ 115 in June to US$ 56 in late December), was one of the reason particularly bothersome for the Russian economy. The cause of the slump in the price included the slowing down of the economy globally (mostly because of the weakening dynamics of growth in China), and also because of the decision of OPEC to maintain the oil production levels despite the falling prices. The changes of oil prices directly impacted the budget stability of Russian economy because the revenues from the sale of petroleum products, oil, and gas accounted for half of the country’s budget. Thus If the oil prices decreased by 1 US dollar in the global market, then the budget revenue of Russia decreased by almost 2 billion USD. As a result of this, the Russian government because of the continuing decline in the prices of oil announced a spending cut of 10% and a budget deficit in the year 2015.

Impacts of the Crisis

One of the major impacts of the crisis was the devaluation of the Russian ruble. Since 1997, Russia took massive loans from the World Bank; IMF etc on the agreement that it would use the money lent by these organizations in order to support its currency but would replay in USD or Euro when it earned rubles, thus giving a stable exchange. Russia was highly successful in doing so and maintaining a steady exchange rate. However, as economic pressure started building up in 2014, it became expensive to maintain ruble’s worth and speculators believed that soon ruble’s value will fall. But nevertheless, the government allowed ruble to float to its real market value, making foreign currencies more valuable. Thus devaluation of the ruble made it very expensive for the people of Russia to buy goods from other countries. Also because of the Dutch disease, the tendency to import rose rather than the tendency to produce. This resulted in a rise in the inflation. Food products witnessed rise in prices. This is because Russia imports most of the vegetables and fruits. Also, because of the devaluation of ruble, producers in the country exported maximum of their food produce, reducing the supply of food products in the domestic market and thus leading to high food prices. This high inflation furthermore resulted in decreased real wages. Unemployment increased in the country and people started fearing to lose their jobs. Businesses which had foreign debt experienced an increase in their debt amount due to the devaluation of currency. (Tracey, 2019) Talking about the “sanction war”, the counter sanctions worsened the situation as Russia passed sanctions against nations who sanctioned it, especially when it came to food imports. All this led to disruptions in the market and high inflation. Also, the devaluation of ruble surely benefited sectors of economy gaining from exports but it resulted in losses in the sectors which are dependent on imports and which have a domestic market. Thus, the sectors using high technology were affected. Energy sector which generated high revenue was negatively affected due to fall in oil prices and lesser exports Sectors like aviation industry, automobile industry and tourism were affected. Moreover, crashing of the Russian ruble led to deterioration of the conditions in which the banks operated and a fall in the listing of Russian assets in stock exchanges, resulting in decline in major investments in Russia as Russian assets became unattractive to the investors. The leading market players also incurred heavy losses due to low capitalization of assets because of the crash of Russian ruble and the tension in relations of Russia with the West. Hence we can say that the financial crisis in Russia had a significant impact on the Russian economy as a whole i.e. at a macroeconomic level.

Empirical Analysis

Data shows that the negative trends in the economy of Russia began in the year 2012 when the economy of Russia reported slower GDP growth for the 1st time ever since the crisis of the year 2008–2009.The GDP growth declined to 3.7% in 2012 as compared to 4.3% in the year 2011. This trend deepened over the years following when the economy of Russia grew only by 1.3%. Even though the price of oil in the global market was still high during the given time-period in, Russia reported one of the least amounts of growth among the emerging economies of the world.

The negative trend of growth continued in the year 2014. Between the first and the third quarter, the GDP growth declined from 0.9% to 0.7%. When Adjusted- for seasonal factors, the growth rate of the year comes close to zero .Decline in investment was also another reason to worry, because investments accounts for 20% of the GDP of Russia. Between January to September of 2014, the investment in fixed capital decreased by 2.5% compared to the year 2013, and the decline of the economy continued in the months after. As in November, the fixed capital investment declined by 4.8% compared to previous year, leading to the breakout of a financial crisis.

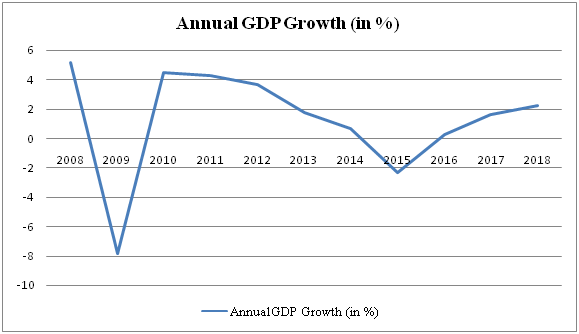

Source: World Bank

The above graph clearly shows the decreasing trend of the GDP growth in Russia from the year 2010. After the 2009 crisis, the annual GDP growth increased but after 2010 it followed a continuously decreasing trend. The annual GDP growth became negative towards the end of 2014 and beginning of 2015 which was when the crisis broke out as is evident by the graph itself.

Also data shows that the rise in the inflation in the country during the financial crisis with the inflation rate reaching the maximum in 2015 at 15.53%. The following graph shows the annual inflation in the country of Russia over the period 2008-2018.

Source: World Bank

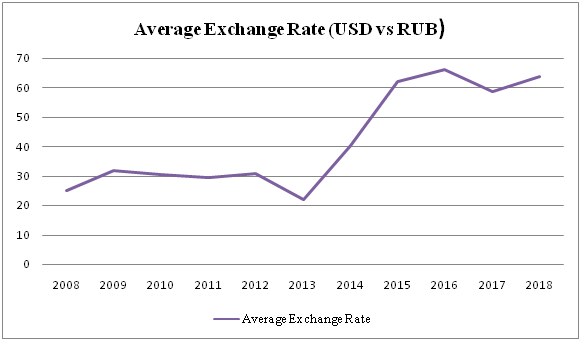

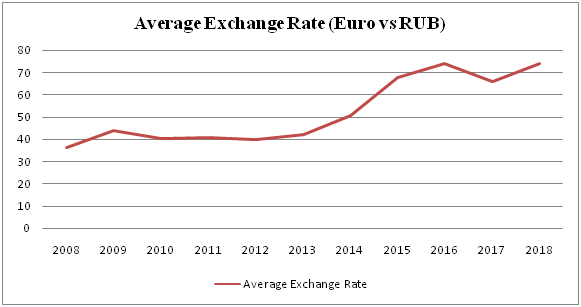

What we also notice is that the fall in the oil prices and a high demand for foreign currencies (USD and Euro) for the repayment of foreign debt resulted in ruble’s fall in value. The following graphs show the average exchange rate (USD vs. RUB and Euro vs. RUB) from 2008 to 2018 and analyze the fall in the value of Russian ruble.

Source: World Bank

Source: World Bank

Government Strategies and Policies

The collapse of the financial market forced the Russian government to make plans of immediate anti-crisis actions. These were designed by the government mainly to uphold the stability of the banking system of Russia and thus the stability and the reliability of the entire Russian economic system. In December 2014, the CBR planned to increase the volume of currency credit available to the banks intending to improve the currency liquidity and easing the limitations imposed on banks regarding setting of interest rates on deposits and loans.

The Federal Assembly of Russia also authorized the proposal of the government for amendments to approve the proposal of providing banks with extra capital of 1 billion ruble. The finance minister of Russia also made an announcement that “the limit till which the Reserve Fund may be drawn upon could be increased multiple times even to as much as 70% of the Funds.” (Osw.waw.pl, 2019)

The government also took various informal measures. It pressurized large businesses to sell a part of foreign currency they earned which included President Putin’s personal “persuasive” phone calls to some large business owners. The government continued to pressurize large companies to keep selling foreign currency in line with a defined schedule till year end while observing the currency operations of the biggest exporters. Moreover, the government decided not to enforce capital restrictions that would eventually tarnish the reputation of the country and its economy in the eyes of the investors.

Moreover, the most important decision that the government made or the smartest strategy that the government adopted was the free float of the ruble to overcome the crisis. Russia lost almost 50% of its value of oil but because of the free float, the government was able to double rubles got per oil barrel. The government also lowered its break even point when it came to oil. It also put away extra earnings into gold reserves and foreign currency. All this helped to stabilize the Russian economy.

Conclusion

The above policies might be effective in the short run but not appropriate for the long run. The depreciated ruble results in exports being profitable but it makes the import of technical equipment needed for Russia’s growth more expensive. Also producing these equipment would be difficult as it would require huge investment which is difficult because of sanctions. This makes all the policies of the government ineffective in the long run. Also, this may raise some other issues for Russia like the need for modernization in production so as to deal with the shrinking of labor force, weakness of the banking sector because of loss in access with the capital from the West, the demographic issue of Russia etc. Thus, the macroeconomic stability in Russia thus depends largely on the dynamics of oil prices, the ability of Russia to maintain currency reserves for foreign debt and the stability of the banking sector.

Also today, we find that Russia is recovering and the oil prices have rebounded. The sanctions from West have weathered along with boost from new sanctions like Iran. All these indicators are positive. But issues like structural issues, instability in banking sector etc still prevails. The Russian government therefore needs to maintain an effective budget policy keeping into consideration the shrinking resources and shrinking labor. Also the credit rating must be taken care of. This is essentially because lowering of the credit ratings would result in massive sale of Russian assets and a large capital outflow.

References

Gylfason, T. and Schmid, M. (1983). Does Devaluation Cause Stagflation?. The CanadianJournal of Economics, 16(4), p.641.

Cooper R.N. (1969). Currency devaluation in developing countries:Preliminary assessment (A.I.D. Research Paper).Yale University

Devaluation, external balance and macroeconomic performance: A look at the numbers.(1989). Journal of International Economics, 27(3-4), p.390.

Bussière, M., Saxena, S. and Tovar, C. (2012). Chronicle of currency collapses: Re examining the effects on output. Journal of International Money and Finance, 31(4), pp.680-708.

Calvo, G. and Reinhart, C. (2000). Fixing for Your Life. Brookings Trade Forum, 2000(1), pp.1-38.

Frankel, J. (2005). Contractionary Currency Crashes in Developing Countries. SSRN Electronic Journal.

Gupta, P., Mishra, D. and Sahay, R. (2007). Behavior of output during currency crises. Journal of International Economics, 72(2), pp.428-450.

Diaz-Alejandro, C. (1963). A Note on the Impact of Devaluation and the Redistributive Effect. Journal of Political Economy, 71(6), pp.577-580.

Blank, A., Gurvich, E. and Ulyukaev, A. (2006). Exchange Rate and Competitiveness of Russia’s Industries. Voprosy Ekonomiki, (6), pp.4-24.

Gupta, P., Mishra, D. and Sahay, R. (2007). Behavior of output during currency crises. Journal of International Economics, 72(2), pp.428-450.

Diaz-Alejandro, C. (1963). A Note on the Impact of Devaluation and the Redistributive Effect. Journal of Political Economy, 71(6), pp.577-580.

Blank, A., Gurvich, E. and Ulyukaev, A. (2006). Exchange Rate and Competitiveness of Russia’s Industries. Voprosy Ekonomiki, (6), pp.4-24.

Osw.waw.pl. (2015). Retrieved from https://www.osw.waw.pl/sites/default/files/raport_crisis_in_russia_net.pdf.

Tracey, G. (2019). How the 2014 Economic Crisis Changed Russia’s Economy. GeoHistory. Retrieved from https://geohistory.today/2014-crisis-russia-economy/.

Mironov, V. (2015). Russian devaluation in 2014–2015: Falling into the abyss or a window of opportunity?.Retrieved from https://www.sciencedirect.com/science/article/pii/S2405473915000379#bib0030

Spence, P. (2014). Russian economic crisis: as it happened 16 December 2014. Telegraph.co.uk. Retrieved from https://www.telegraph.co.uk/finance/economics/11296233/Russian-economic-crisis-live.html.

Informative!

LikeLiked by 1 person

Nice

LikeLiked by 1 person

Insightful!

LikeLiked by 1 person

Amazing

LikeLiked by 1 person

Kudos!Good work…very educative.

LikeLiked by 1 person

Very goood

LikeLiked by 1 person

Great piece of work

LikeLiked by 1 person

Great research

LikeLike

Can be used as an basis of propaedeutic.Must say very well researched and very informative.

LikeLiked by 1 person

Great blog. Really informative. Good job.

LikeLiked by 1 person

Really a great insight into Russian’s federation crisis.

LikeLiked by 1 person

Well done, good researched beta.

LikeLiked by 1 person

meticulous research work.

LikeLiked by 2 people

A very good analysis of Russian economic crisis caused by the decreasing oil prices in world market in2014 and economic sanctions by the west on Russia.

You have given its impact on the Russian economy and the remedial steps taken by the Russian reserve bank.

This is a established fact that the economy has to face turbulence and the the direct impact will be on the people of that country in the given circumstances.Only a economy which is self dependent on its internal resources can survive.

LikeLiked by 1 person

Great article and really very informative. Always interested to know and read about Russia which makes this article very insightful

LikeLiked by 1 person